Let me help remove the rose-colored glasses for anyone who still thinks GDP this year is good.

First, GDP growth in the first quarter was not “great” as I’ve heard some claiming. It was, by US historical standards, a little lower than mediocre. Second, the biggest tax cuts in history only got us down to 2.9% GDP growth for 2018. GDP growth had been pegged originally around 3.1%, but that was revised down, as is usually the case. Every administration tends to estimate GDP on the rosy side because bad news is swallowed easier the further back in time it lies. So, estimate high and revise lower seems to be the government’s perennial approach.

If you revise the number down after a little more the time has passed, people don’t care as much because they are now focused on the new number for the latest quarter. Revising actual GDP (not just the headline growth number) from past quarters down also makes it easier to show more growth in the present quarter. That means we are likely to see the second quarter’s number of 2.1% revised down to something like 1.9% when the third quarter comes in. That’ll make it easier to make the third quarter look a skosh better than it otherwise would.

Either way, the latest number is far from being the “healthy pace in the second quarter” that one market commentator I read recently claimed we just saw. A reading around 2% is actually a pathetic number for a number of reasons. When I was young, we considered that a pre-recessionary number. It was an amber light that said the economy was going soft.

GDP growth looks worse in context

It is when one considers all it took just to get us to this 2.1% growth, that GDP growth looks particularly pale compared to most years since the Great Recession. 2018 was the year of our discontent when the stock market crashed to a bear that is still growling around the market (what with Morgan Stanley saying 80% of the indices it monitors remain in bear mode since last year). Yet, 2018 was the first year of the most massive trickle-down tax cuts in history — bigger than the Reagan trickle-down cuts and bigger than the Bush trickle-down cuts! That makes 2.1% GDP growth a truly milquetoast number at best.

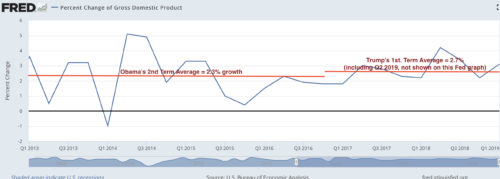

Add this to the context: We got there after government “stimulus” spending that put all other deficits in the past to shame. We ran the largest deficit the world has ever seen during a time that was already growing at 2%! We’ve gone exactly nowhere since Obama who also averaged around 2% GDP growth. (See graph above.)

With so much government deficit spending, particularly in the corridors o military-industrial complex, it should have been easy to accelerate the US economy like a rocket ship, as Trump has claimed we could have done with the Fed’s help. Sure, we have had slightly higher deficits when trying to engineer our way out of recession (even then only once), but this deficit came after years of supposed “recovery” when we were already growing with unemployment already at all-time lows. It should have been rocket fuel. And we got nothing!

We poured fiscal gasoline on the entire economy and hit it with a flame thrower, and this 2% GDP growth is all we got for it! That is worse than no bang for the buck! We actually got a decline from the second-quarter growth rate a year ago! In fact, we are essentially right back where we were on the day Trump took office.

All of this speaks to how badly the Fed’s recovery failed as soon the US economy was taken off Fed life support because that is the big force that coincided with all those tax cuts and that stimulus spending. Throughout 2018, the Fed kept raising interest rates and reducing its balance sheet.

Being certain the Fed’s attempt to “normalize” the economy would create a downdraft so massive it would even overwhelm the Trump Tax Cuts and Trumpian-sized stimulus spending is why I have referred to this period as the Fed’s Great Recovery Rewind. The economy spiked briefly then sank rapidly right back to where it began, and the stock market crashed. One might look at it this way: even the new support of mammoth corporate tax cuts and stimulus spending couldn’t save the Fed’s fake economic recovery once the Fed removed its artificial life support from the economy.

The trickle that didn’t

It is not, however, simply that the Fed failed, as Trump would like to place the blame. Putting tax cuts on the supply side (in the hands of the rich) does not stimulate the economy. It stimulates the stock market and drives up asset prices. The Fed has stated that it intentionally orchestrated its money creation to channel through the supply side as well in the hope that driving asset prices up would cause capital investments, which would stimulate the general economy. So, the Fed backed off its supply-side supercharger at the same time the government kicked in supplyside stimulus.

What we saw during the Fed’s supply-side biased stimulus, however, was that almost all of its new money remained in the hands of stock holders. As far as I was concerned, it was a foregone conclusion that it would. Here’s why: If you put all of the tax cuts on the demand side, there would be only one way the rich could get their hands on those tax cuts. They’d have to make things and market them to entice the demand-siders to spend their tax savings in the direction of the rich.

Do you think the rich would just ignore this potential for new markets? If they did, I can assure you entrepreneurs would rise from among the poor to seize the day. Because the demand side (the consumer side) was empowered by the tax savings, they’d be able to demand the products the rich or the new entrepreneurs try to entice them with. That is the only way the rich would have reason to build factories and hire more people.

I guarantee you, tax cuts will always bubble up to the higher strata of society more readily than they trickle down. Far too many filters stop up the channels on the way down for anything more than the slightest trickle to make it to the bottom tiers — not even enough to slake your thirst.

Don’t you find it contradictory that we consider the US economy’s greatest strength to be the consumer and, yet, we repeatedly make sure the consumer who drives the economy gets the least of the tax cuts? That strikes me as the kind of self-contradictory thinking that can only be explained by greed.

If you think 35 years or so of repeated episodes of supply-side economics have trickled down to the demand side of the economy, you might want to take a look at how the average consumer is really faired over that span of time in this last article I wrote: “Bubble Bubba Isn’t Doing Fine Anymore.”