You may be worried my prediction that a recession will start sometime this summer is not looking too good. So was I after first-quarter corporate earnings started coming in better than what economists expected. Except that barely “beating expectations” is kind of pathetic when expectations are dumbed down as far as they were.

(Note that I have also stated each time I repeat this prediction that we won’t know until half a year beyond summer whether or not it happened, because initial GDP reports are often revised down after the next quarter (perhaps in order to make the next quarter look better quarter on quarter) as facts come in more clearly and because no recession is officially declared until a month after two full quarters have seen total GDP decline — not a decline in the growth rate, but an actual drop in GDP.)

What does it really say that the new gauge for earnings is whether or not they are better than horrible? (Forget about growth. Earnings were actually downan average of 3% YoY, meaning they may already be deep in recession.) Of course, we also have to factor in those continuing record stock buybacks that reduce the divisor in the earnings equation. And while I have not made any predictions for the stock market this year, we have to factor in the reality that the cash from foreign-profit repatriation, which has been fueling many of the recent buybacks (now that money is no longer on loan for free) is going to dwindle away this year, though it is holding up longer than I thought.

With all stock indices essentially back up to their previous two summits, I believe they will starve for air in this stratosphere and will start to fall back down again soon — probably back to where they came from in December, maybe even punching a deep hole through that floor. In fact, if you look back over my past predictions for the stock market’s crash, it’s clear I believe it will go down a lot further than it has so far. (It’s 2018 crash would have already gone down there if not for the Fed rapidly abandoning its long-stated plans.)

HOWEVER, whether or not stocks drop further, their rout is not my focus this year because it is almost irrelevant as to why we are going into recession unless stocks decide to make themselves relevant by driving us there more quickly. In the very least, stocks will eventually follow.

My point is that we are likely going down the recessionary hole this year, regardless of what stocks do. (See my article referenced above for those reasons.) While I do not believe in my recession timing as completely as I did my timing for the stock market’s crash last year — and, in fact, am not certain of it at all — I still think it is our most likely path for the year. I wouldn’t bet my blog on it as I did with stocks last year because my timing is much earlier than anyone else’s; so, once again, I am out on a limb by myself.

Here is something to bear in mind: Regardless of what stock averages are doing, the major corporations that are likely to be harbingers of what is coming for the general economy are foreshadowing, as I reported in my last article, darker times ahead.

Exxon, which broadly reflects the critical central role energy plays throughout our economy, just pulled a 3M face plant. These are some major downbeats. Exxon reported a MASSIVE 50% drop in profit, and that fell far short of lowered expectations. (60% drop quarter on quarter.) Its stock, however, only dropped 2.7% for the day, a mere jog compared to 3M’s cliff dive the day before.

So, neither individual stock prices nor stock indices are reflecting everything the companies, themselves, are reporting because stock prices don’t have to go where companies go. All the euphoria and denial in the stock market — built in from years of just following the Fed’s money — along with all the buybacks that shunt the equations — make stocks right now a poor gauge of where the economy is going. It is more likely the stock market will wind up playing catch-up to a recession as denial continues to rule the day so that stock prices are far from pegged on the fundamentals of their companies any longer.

The stock indices are outstanding (up to the moment), in spite of clear warnings from some key companies — most notably Intel (down 9% on Friday), 3M and Exxon so far — that should not be ignored (not so much for witching where stocks are going but for seeing where the economy is going or, at least, where it went in the first quarter). More importantly, the forward guidance from those companies is even worse than their first-quarter results.

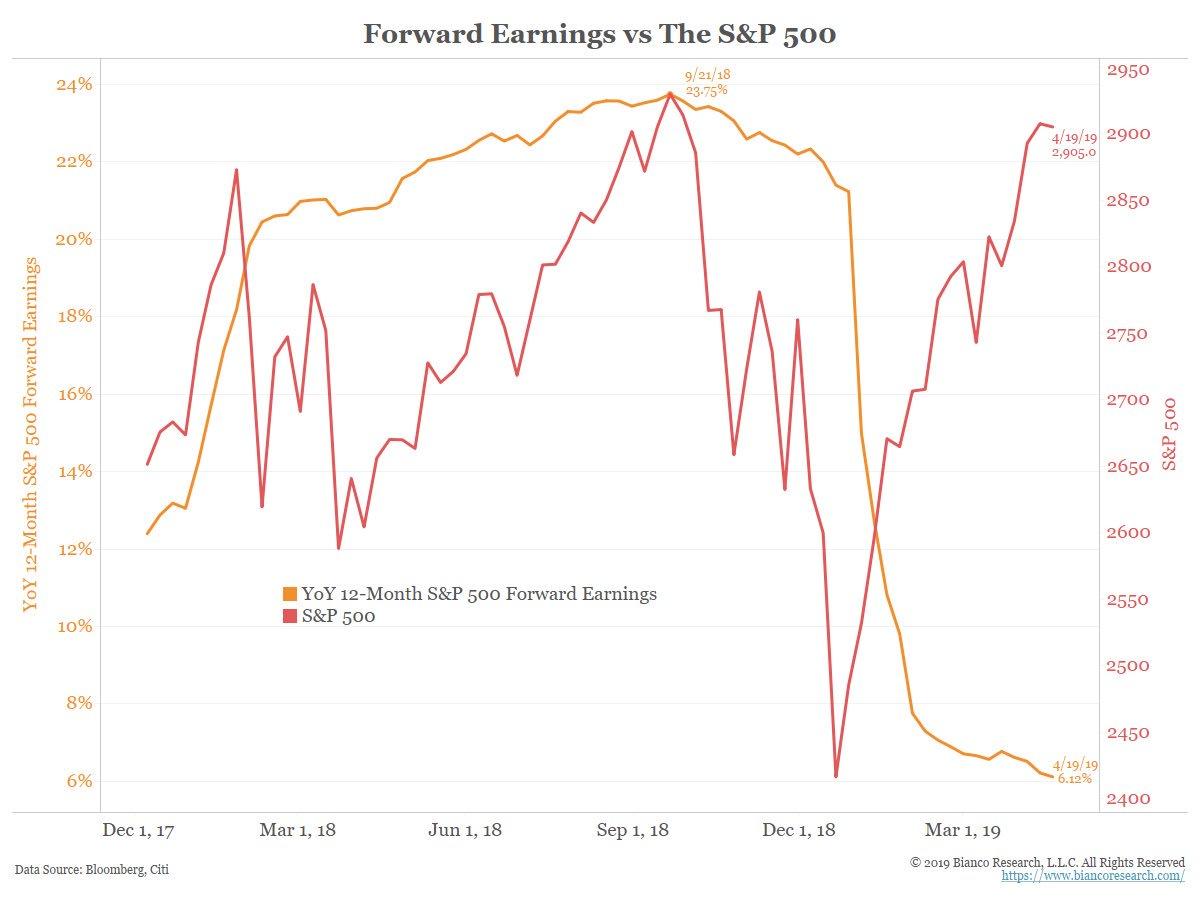

Here’s an interesting little graph:

That makes sense, right? As forward-looking earnings expectations plummet, the S&P 500 skyrockets? Sure it does.

Consider also that corporations have increasingly been noted by many mainstream commentators over the past few years as reporting a lot more blue sky than the old GAAP standards for accounting allowed. Accounting gimmicks have become standard reporting practice, leaving our stats not much more reliable than China’s.

Bottom line: stock prices cannot be seen as a reliable indicator of where the economy is going when they are not even a reliable indicator of where the actual economy has already gone and when they run totally counter to what corporations are reporting as their forward expectations. As a result of years of Fed interference, stock prices have become completely unhinged from economic reality. That doesn’t mean they will fall. It just means they bear no reflection of the economy … at least not until reality rips into them so severely they cannot withstand it. (I don’t even know if that can happen any more, but reality does have a way of eventually overpowering delusions.)

GDP roars like a mouse

Unlike stocks, GDP is exactly where recessions are measured, so what happens there is highly relevant to whether the economy is sliding in the direction of my prediction. However, GDP is government baked, and includes a lot of assumptions and “adjustments” that are often made of rose water. Nevertheless, it is the only yardstick people will accept for measuring a recession. So, I’m stuck with it.

That is why the GDP spike back up to 3.2% growth on Friday raised even more concern within me that I might prove wrong about the recession that is building. Suddenly the GDP tachometer shows the economic engines have roared back up to cruising-speed. Highly doubting all the noise that emerged, I looked under the hood to see what was powering it all.

Not too impressive! A bunch of rats in a hamster wheel.

My prediction, while it places a recession sooner than anyone else I have read, may be safe. (For the moment, I wipe my brow, but I don’t settle easily in the position I’ve taken.) Even though GDP growth came in stronger than anyone expected — at least in the headline number — the data have some serious weaknesses.

Talking inventory of the GDP report

First and foremost, the apparent burst of renewed strength can be attributed primarily to a rise in inventories (a nearly 30% leap) and exports …

that analysts say aren’t likely to continue in the year ahead, potentially setting the stage for weaker economic growth in the quarters to come.MarketWatch

While I often don’t put much “stock” in what analysts say, I will note that inventories are not likely to grow any more because that 30% jump leaves them looking backed up. At the same time, consumer growth was actually a weak point in this GDP report, meaning some inventories are likely to back up more. When the nation’s economic growth, as reported, is happening in inventories, it can actually mean the economy is slowing!

After stripping away transitory factors, the economy actually slowed markedly in the first three months of the year…. GDP also was flattered by a sharp jump in inventories, which added 0.7 percentage point to the 3.2% figure. Government spending also surged at a 2.4% annual rate, reflecting a jump in highway and road spending, reversing a 0.4% contraction in the fourth quarter. Stripping out the government, trade, and inventory swings, real private domestic final sales—the core of the economy—grew at only a 1.3% annual rate, half the pace of the fourth quarter. That was the weakest rate since the second quarter of 2013, Morgan Stanley economists write in a research note.Barron’s

Whether a backlog in inventory develops or not, a large build-up in inventory usually comes from bringing sales forward on the manufacturing end, which typically ends in a slow-down in production shortly thereafter:

The boost from inventories in the March quarter points to downside risks for the current quarter, the bank’s economists further point out. Indeed, this was the third consecutive quarter in which stock building boosted GDP. Now comes payback time. Morgan Stanley is looking for a large GDP reversal in the second quarter, with its economists forecasting a downshift to just a 1.1% pace.

And by saying stock-building boosted GDP for the third consecutive quarter they do not mean that GDP increased for three consecutive quarters; they mean that it would have fallen even more than it did if not for this buildup in inventory that gave enough boost to soften the fall. They are now saying this boost has likely run about as long as it can before the inventory buildup turns into back pressure on manufacturing.

Government picks up the tab

Second, the biggest contributor to GDP’s rise was state and local government spending, which also doesn’t mean the general economy is doing better, though some will hope that more government spending will boost the economy, and it certainly boosts GDP … by popping up 3.9%.

So, state and local governments may be the undoing of my prediction when they pitch in at this level, if the money is going into construction, which drives a lot of other economic activity. And that is where a lot of it is going. However, that does not seem to be helping the average “consumer” so far:

Fed up with consumption reports

Sales to domestic buyers saw their weakest results in three years, and consumer spending saw its smallest gain in a year. Growth in business investment and construction also slowed, and housing investment went backward.

For a different look on how the consumer is faring … mortgage originations at Wells Fargo…, the nation’s fourth largest bank by assets, declined 23% year-over-year in the first quarter and 18% at JPMorgan…, the nation’s largest bank by assets. In fact, revenues at Wells fell across all business lines with profits only coming as a result of cost reductions….

Let’s keep this simple and just look at growth in the major parts of the private sector on an annual basis – consumer spending, housing, nonresidential construction, business capital spending:

Q2 2018 4.0%

Q3 2018 3.0%

Q3 2018 2.3%

Q1 2019 0.9%

Tell me again how the economy is growing like gangbusters?Seeking Alpha

Residential construction dropped 2.8%. That is its fifth consecutive quarterly decline! (Does my solitary “crow on a wire” still think I was wrong at the start of last summer to state before anyone else that housing had turned a corner and was headed into a protracted decline? If so, good luck with actually making your case, Crow!)

Personal-consumption expenditures—which account for more than two-thirds of the U.S. economy—slowed sharply in the first quarter, to a mere 1.2% annual rate from 2.5% in the fourth quarter of 2018 and 3.5% in the third quarter. “Consumption was likely held back in the first quarter by a number of headwinds including the government shutdown, poor weather, and market volatility at the very end of last year, and so we would expect a healthier pace of spending next quarter,” the bank’s economists write.Barron’s

Sure, that could be just weather. We won’t know until the second quarter comes in, but disposable personal income was also reported to be its weakest in a year and a half; and UPS reported profits were down 17%, mostly due to a fall in revenue, which backs the government’s overall consumer data. However, this, too, was blamed by the spiked-rose-water-drinking economists on bad weather making package delivery difficult.

All I can say is, “We shall see.” It seems to me UPS got all of its packages delivered. Are we to assume there were a lot of packages heaped up in the warehouses in April that they couldn’t get delivered in the first quarter? Or are we to assume people ordered less just because delivery would be difficult for UPS? Or did UPS just throw a lot of packages over a cliff because they couldn’t handle them in such bad weather. If the weather was bad, wouldn’t more people shop by mail to avoid going out in the bad weather themselves? Wouldn’t bad weather cause more items to ship by UPS so UPS can do the driving.

It doesn’t seem to me that the holiday season has ever proven slow for UPS just because the weather is worse at that time of year. It does seem to me, however, that the only economists who get reported are the ones who wear sunglasses indoors because everything seems so bright to them all of the time.

(I guess I did have more to say than “we shall see.” Sometimes just seeing all the economists in their party hats exasperates me. It’s hard to believe so many supposedly smart people can can act so stupid by merely parroting everyone else’s lemming-brained drivel. Still, that’s why I’m here, writing to lay out logical perspectives you cannot easily find elsewhere and to strip the fake gloss off the frosting put out by economists who have damaged their eyes from staring at the sun. I understand looking at the bright side, but not to the point of losing your vision.)

Let me demonstrate the insanity via Barron’s:

Talk of an earnings recession is so last-week. With numbers in for just over 20% of S&P 500 members, the latest growth prediction stands at negative 3.3%. That’s as good as a gain, and it pushed market indexes to new highs on Tuesday.Barron’s

It is? Do these people even read themselves?

Two things we knew going into reporting season were that the earnings growth consensus stood at negative 4.3%, and that companies would surely surprise to the upside.

Woohoo! So, the fact that actual reported earnings improved from a estimated decline of 4.4% to estimates now that earnings will end up declining 3.3% in aggregate by the end of the reporting season is same as a gain? Geeze, let’s guess they’ll be down 10%, and then we can exult when they only crash 5%!

I can understand that stock prices go up when the market has already priced in worse predictions that don’t materialize; but to call the backsliding in earnings that does materialize the same thing as a gain??? It certainly doesn’t reduce the risk of an earnings recession any. A 3.3% decline (negative growth), if that is where the reporting season ends up, means it appears an earnings recession has already begun, depending, of course, on how next quarter turns out (given that even an earnings recession is typically defined as two quarters in decline).

But everyone is happy, so I guess recession is so last week. Keep on moving, folks.

To end it all simply (or just to end myself after hearing that), the underlying domestic data look perfectly primed for a downturn.

Finally, inflation also fell back sharply from 1.9% annually to an annualized 1.4%, which is certainly an economic change more typical of a looming recession than a hotly expanding economy. In the very least, the dive in inflation looks like it is time for the Fed to cut interest rates again just to drive inflation back to the Fed’s 2% target. Oh, hold it. The Fed only starts doing that when the economy is going into recession! Liked it?